Through our Tuesday TouchPoints series, we are sharing a diverse set of content we hope will be helpful to those managing through volatility, working from home, or just connecting.

By Meka Millstone-Shroff

One thing for certain during this very uncertain time is that the retail world will never be the same.

Prior to this pandemic, the vast majority of retailers were already deep into efforts to transform the way they thought about and conducted business in order to thrive in the increasingly digital age. Retailers do not have a choice to go back to ‘business as usual’ pre-COVID 19, as that ‘normal’ was already on the endangered list and has now crossed the threshold to extinct.

Given the current crisis, what elements of retailer transformation efforts will accelerate, and what will be the impact to the way consumers shop? Which will decelerate? What new thought processes need to be taken into consideration, and what of this will be a temporary new normal versus a more permanent part of the retail landscape in a post-pandemic world?

TRENDS THAT WILL ACCELERATE

Changes In The Way Retailers Operate

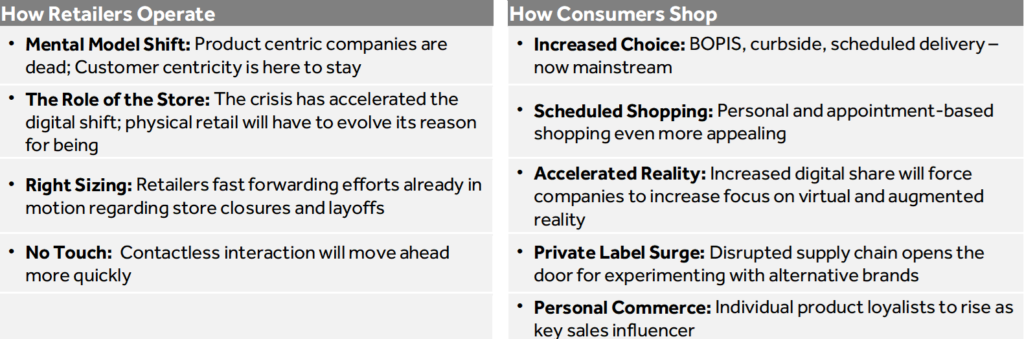

1.) Complete Mental Model Shift to Customer Centricity (Product centric companies are dead)

-

- This trend was already evident pre-COVID 19, but because of the crisis, now more than ever, retailers need to have a clear vision of why they exist. To be successful, retailers need to be able to answer:

- What role(s) do you serve in your customers’ lives? Why do they need you?

- How can your products and services help your customer live a better life?

- As events unfolded it became clear retailers would need to shift their messaging to consumers overnight to flex strong empathy muscles, or risk coming across as clueless and self-interested if they continued with regularly scheduled marketing programming.

- With a slow-down in discretionary spending, retailers have put more emphasis on staying relevant via content and community, focused both around how customers can get the most use and enjoyment out of past product purchases, as well as tapping into the broader life objectives their customer base is trying to achieve via these products (e.g., be the best parent they can be, explore their creative potential, improve longevity, celebrate moments big and small, etc.). Retailers would be wise to continue this focus – positioning themselves as an experienced friend with the same passions, not a company pushing products for their own benefit.

- Doing your homework and immersing yourself in the customer’s mindset using multiple methods is always an important foundational element of being customer-centric. Unusual events at this mass scale, allow for potentially interesting data insights, e.g.:

- What did customers stock-up on, suggesting they cannot live without?

- When faced with an out-of-stock favorite, where were customers willing to try substitutes vs what did they pass up as an acceptable alternative?

- What new products were adopted? What was deemed as unnecessary?

- This kind of sales and inventory data analysis, combined with the focus above of thinking through your company’s role in helping your customer achieve a life objective, can help inform how you merchandise your products into holistic solutions that make it easier for the customer to understand what you stand for and how you can help them.

- The requisite shift to a customer-centric mindset is ultimately a part of the larger societal mandate calling on companies to move from “Purely Profit” TO “Purpose + Profit”

- This trend was already evident pre-COVID 19, but because of the crisis, now more than ever, retailers need to have a clear vision of why they exist. To be successful, retailers need to be able to answer:

2.) Increased Digital Share Forces New Roles for the Store

-

- Ecommerce was 16% of US retail sales in 2019, having grown 1% a year over each of the past 10 years. Starting in the latter half of March 2020, this metric will be in for a wild ride and is now projected to grow another 10% this year alone to a 25% penetration.

- While retailers were partaking in transformations over the last 5 to 8 years, no one knew exactly what the answer would look like ‘out the other side’, but one thing everyone agreed on was that the winning answer would be omni-channel. Retailers (whether in the traditional sense, or DTC) would need some combination of both a digital and physical presence.

- Digital share just got a major rocket boost that is likely to have some staying power, especially in categories like grocery where new customer segments were forced to give it a try.

- While there might be some pent-up demand for physical shopping as a form of entertainment, recapturing foot traffic will likely be slow, especially for some categories (e.g., apparel, which has been hit particularly hard by the crisis, may find that customers are wary of trying on clothes that could have just been tried on by others and may prefer the more sterile look of online shipments – a more costly outcome for these brands).

- Nevertheless, physical retail won’t and shouldn’t go away. Smart retailers will re-think the role(s) of the store and store associates – from enabling ship-from-store, facilitating the returns of online-only players, to doubling-down on human interactions that are difficult to replicate online (e.g., expert help identifying multi-product solutions to a tricky problem), to thinking of space and people usage differently (e.g., offering up trunk show space on a rotating basis to DTC or multi-level marketing brands relevant to your customer and your brand; enabling in-store associates to service online customers when traffic is low in their location, etc).

- Shopping feeds several human needs from serving as a form of entertainment or social activity (how many of us would love to peruse any non-essential store at this point, just to get out of the house) to a source of discovery and inspiration, to expert affirmation on product decisions, as well as good old-fashioned sensory pleasures and self-indulgence. While some of these needs can be met virtually, sometimes you just can’t replace the energy you feel from interactions in an environment filled with others.

3.) Right-sizing: Pulling Forward Store Closures (& Layoffs)

-

- Even with re-imagined roles for the store, this crisis provides a window of opportunity for retailers already at the knife’s edge to fast forward their right-sizing efforts.

- Brick & Mortar: Retailers usually consider store closures in batches based on timing of leases coming to an end. Given forced temporary closures, retailers are trying to negotiate deferred or even waived lease payments with landlords and developers across the country. It’s in the interest of landlords to be open-minded vs risking spots going dark, putting them at risk of tripping co-tenancy clauses in other lease contracts. Retailers can now make some early closures part of a deal in paying to keep other locations open.

- Employees: Unfortunately, similar logic holds for layoffs. Retailers that were already seeking cost savings to right-size their balance sheets have now been put in the position of having to furlough a significant portion of their workforce both at the store and corporate levels. Some have even done layoffs and more are likely to come as retailers continue to assess the evolving landscape

4.) Contactless Payments – Mobile Tap, No Signature Required, & Self-Checkout

-

- With widespread fear of germs from touching keypads or pens, the adoption of contactless technology, from both the consumer and retailer sides, will be put on fast-track (and perhaps the US will finally catch up with the rest of the developed world). We’ll also start to see more contactless loyalty abilities where a customer does not need to provide any information to earn rewards, receive email receipts, or auto-enroll in rebates, warranties, and recall information (e.g., via new fintech companies such as RotoMaire).

Changes In The Way Consumers Shop

5.) More fulfillment options – BOPIS, Curbside Pick-up, & Scheduled Home Delivery

-

- An obvious silver lining for retail was how quickly businesses were able to mobilize to begin offering new pickup and delivery options. Many of these were initiatives that were on retailers’ to-do lists for years, but never rose to the top as a priority. With the sudden crisis, and basic operation of physical stores completely stopped, retailers (from large chains to mom & pops) were able to ‘figure it out’ seemingly overnight in order to salvage any sales possible.

- While many of these new services were made possible via “bubble gum and band-aids”, the consumer desire for them is obvious and will not go away. We will continue to see more fulfillment options (e.g, back-orders) and more flexibility for scheduling desired delivery/pick-up windows.

- Speaking of which….

6.) Growth of Appointment-based Shopping

-

- …we were already starting to see an increase in personal shopping services (e.g., stylists, decorators, registry consultants) that allowed a customer to reserve a specific shopping timeframe, accompanied by an expert that would help them choose the best products for them.

- Starting with Best Buy’s announcement in late April that they plan to slowly re-open stores via appointment-based shopping, we’re likely to see more both as a way to control social distancing, as well as a way to grow basket size and increase customer loyalty.

7.) More Investment Into VR and AR

-

- Many have predicted the explosion of virtual and augmented reality for a while. Technology, including the ongoing ability to quickly and cost-efficiently create digital assets (e.g., 3D models), are still not quite where they need to be. With increased digital share, there will be more incentive for companies to invest in these capabilities.

8.) Private Label Penetration in Consumables

-

- As customers made a run on stores early in the COVID crisis, supply chains for many basic items have been challenged. The good news for retailers is that given the perceived or real urgent need for these items, consumers are willing to experiment with brands they had not considered before. So if Charmin’s toilet paper (or insert any other brand name consumable from disinfecting wipes to hair color to dish soap) were out-of-stock, why not try the store’s private label brand?

- Once a customer tries your private label, they often won’t go back. That’s because private label products are not only a percent margin win (and often absolute margin dollar win) for the retailer, they are also a better value for the customer. Good news all around (well, not for the big brands, sorry).

9.) The Rise of Personal Commerce

-

- Going into this crisis, the gig/freelance economy was already strong and getting stronger. With so many people’s income impacted by the crisis, many are looking for additional ways to earn money (we see it in the increase over the last month in the number of people who have signed up to be consultants in multi-level marketing companies, such as Beauty Counter). Combine that with brands and retailers whose main go-to-market channel has been shut down, and you create the opportunity for a new sales channel – personal commerce!

- Providing loyalists the ability to act as an extension of your salesforce will grow in popularity. The world is recognizing that everyone can be, and is an influencer amongst their own circle of trusted friends and family, whether or not they have the desire to create content (especially now that mega- and macro-influencer programs are getting pressured as celebrities/influencers are experiencing backlash for any display of wealth/privilege). Personal commerce SaaS platforms are emerging that enable any company to finally launch an ambassador program that will work, directly rewarding individuals for the conversations they’re already naturally having. These platforms (e.g., start-ups like Plazah) will also empower the company’s experts to provide personalized recommendations to existing clients or new online shoppers, from the comfort of anywhere.

TRENDS THAT WILL DECELERATE

Changes In The Way Retailers Operate

1.) Experiential Retail – Great Idea, Just Not Now

-

- Figuring out how to turn in-store shopping into more of an ‘experience’ to drive customers off their desktop/phone and into stores, has been a major quest for some time. In-store shoppers typically spend more than online shoppers, partly due to impulse buys (which is why retailers like getting you in the store via BOPIS), as well as increased basket sizes from easier browsing ability and interactions with associates or product displays that can lead to cross-selling and trading-up.

- Many of these in-store luring tactics will unfortunately be put on hold due to sanitation and distancing concerns:

- Food samples and cooking related demos (that free lunch you used to get walking around CostCo on a Saturday afternoon is going on a long hiatus)

- Beauty-related testers (there goes half the fun of Sephora)

- Interactive product displays (wait what? Apple stores have been heralded as the holy grail of in-store experience! Perhaps they’ll just implement requirements that customers wipe down each device after playing with it, much like good gym citizens are expected to wipe their sweat off cardio equipment.)

- Events – a packed store buzzing with human energy (and potential germs) may not be so appealing for a while

- Instagram-able pop-up experiences (e.g., Candytopia, Happy Place) – the sanitation level of many of these experiences were unfortunately the adult equivalent of toddler ball pits

2.) Thinking Global Shifts to Thinking Local

-

- Tariffs already caused many retailers to look to diversify their supply chain out of China. With countries (or even US states) shutting down at different periods of time, companies were at their mercy. As a result, many companies will look to bring parts of their supply chain more local (regional and national counts; certainly more will continue to move out of China) or more directly in their control.

- A lot of international politics and global tension will come into play here that will have implications on retailers and other businesses, but I won’t go there.

- There will be other not so obvious implications of bringing more elements back into a company’s own control. For example, warehouse space might increase, both as retailers build more safety stock and as they shift some vendor drop-ship items to stocked inventory. In communities that can afford it, there will also be an increase in the desire & supply for “Made In America” goods, especially those made more local to each community.

Changes In The Way Consumers Shop

3.) Experiences Over Things Still Relevant, Just Now Things Needed To Create Experiences At Home

-

- It’s not just toilet paper that is out-of-stock, it’s also weights/gym equipment, Nintendo Switches, yeast and bread machines, bases to make your own body butters and scrubs, etc.

- While fear remains in some portion of the population, capacity restrictions prevent people from making the reservation cut for eating out, or large gatherings like sporting events and concerts are not allowed at all, Americans will continue to get creative in how to spend their time. We will see a renewed appreciation for experiences that occur in the home with close family & friends (e.g., family game nights, movie nights, theme dinner clubs) and new hobbies (e.g., veggie garden with the kids, new musical proclivities, etc). Many of these will result in increased spending on ‘things’, while we continue to see a decrease in spending on out-of-the-home experiences that typically have large crowds or trap you in a confined space (e.g., ticketed events, museums, amusement parks, cruises, airline travel)

4.) Realization The Everything Store is Not Everything

-

- The first two decades of the 21st century were marked with massive SKU proliferation (as retailers built out never-ending digital aisles, encouraging vendors to build drop-ship capabilities, unknowingly eliminating barriers-to-entry for new online competitors), fast fashion, the explosion of DTC brands, and of course, the monolithic everything store.

- Yet more is not always more. Some of the digital capabilities that were envisioned to level the playing field, have also brought forth a whole slew of actors taking advantage of others, with none of those big enabling platform brands doing anything to truly vet their ‘partners’ before facilitating interactions with their world of trusting consumers.

- Whether it’s a digital ad linking to a product company that doesn’t actually ship anything, or receiving a product ordered from a 3rd party marketplace seller only to find it’s a piece of crap, people are beginning to realize they value what used to be the main role of the retailer – Curator. e., someone whose job it was to actually vet the products they present for sale, acting as an agent for the customer.

- People will want more transparency regarding from whom they are buying (which does not mean more star ratings which could have been paid for or generated by the seller themselves) and from where the products are coming. Brands that have a knowable story will start to matter more. Just how long they will have to pay the toll to the players that built the infrastructure to draw attention to their story in the first place, is a question that should be examined more closely.

NEW TEMPORARY NORMALS

Changes In The Way Retailers Operate

1.) The Obvious – New Cleaning and Distancing Standards

-

- As stores are slowly allowed to re-open, retailers want to protect both customers and employees. Several new cleanliness and distancing standards have already appeared in essential stores, such as:

- Store capacity constraints

- Markings on the floor to specify traffic flows and to delineate safe spacing at checkout

- Workers provided with and required to wear masks and gloves

- Customers required to wear masks

- Customers greeted with a sanitizing wipe for their cart; some retailers will even go so far as handing out gloves (while costly, this effort increases customer trust in how seriously the retailer is taking the sanitation of its store)

- Plexiglass shields at POS

- More rigorous and more frequent cleaning schedules (as we all know from the 100’s of emails we received from every email list we subscribed to in early March, before they were all forced to close)

- We’re also likely to see the introduction of:

- UV lights for periodic sanitization, when the store is empty of customers

- Contact tracing notifications as technology is made available to identify customers and employees who were in the store (or used the same POS terminal) as someone that has tested positive for COVID-19

- Most retailers can’t afford the incremental costs of these initiatives on an ongoing basis. Companies want to do the right thing protecting the health of their local communities, they want to engender trust from their associates and their customers, and they want to protect against another possible forced closure, but how long these new standards will be in place is a great question.

- As stores are slowly allowed to re-open, retailers want to protect both customers and employees. Several new cleanliness and distancing standards have already appeared in essential stores, such as:

Changes In The Way Consumers Shop

2.) New Habits of Consumers Stocking Up on Key Items, Along with New Conservation Awareness

-

- Some of the hoarding behavior, caused by pandemic-related anxiety, will continue beyond what seems necessary. As people have tried to cut-back on their number of exposure-risk shopping trips, combined with sometimes finding several of the items on their list out-of-stock, customers will continue to buy more than their typical quantities when they see basic items or favorites available. (The trend of people moving out of urban areas to suburban, and from suburban to rural, also helps with providing more space for all these extra goods.) Unfortunately, this behavior causes a self-reinforcing vicious cycle at scale.

- Given many companies are operating at lower capacity or lack critical inputs in their supply chain, supply can’t seem to keep up or get ahead to build confidence back into the system.

- As a result (and as part of that pandemic-related anxiety), we’re also seeing more awareness of waste at a consumer level. Many consumers are demonstrating depression-era like frugality such as re-using plastic sandwich bags and tin foil, or getting creative with using up all pantry items (almost like they’ve been challenged to an episode of Chopped). Of course, in the big picture this is a good thing.

- While some grocery stores have reversed policies for the time-being, in terms of not allowing customers to bring in their own re-useable bags, or people are using more single-use/disposable plastics (even if just to cut down on their dish washing time), there’s hope this crisis is drawing more attention to our collective impact on the world around us.

- With news that you can finally see the skyline in typically polluted cities, or even just enjoying the peace from less traffic noise, people are questioning whether this virus was a wake-up call from mother nature. While many have expressed support for sustainably made goods, few in the past have been willing to pay up for it. In theory, there will be more support, but with a recession (if not potentially a depression) ahead, consumers are not likely to put their money where their mouth is, unless the product is available at parity in both price and quality.

Whether our future looks more like a scene out of “Minority Report” or the devastation of “Ready Player One,” what happens to retail matters to everyone. Not only does retail shape the personality and landscape of our communities, retail also supports employment for almost 10% of all Americans. The future of retail has broad-reaching impact in our circle of economic life. Retailers, just like everything governed by the laws of nature, must evolve or die. On top of that, fundamentally retailers are intermediaries, and all intermediaries eventually get dis-intermediated unless they are contributing a specific unique value. Here’s to placing my bet on retailers rising to the challenge of our new normal.

Meka Millstone-Shroff is an HPA friend and retail executive with over 20 years of experience growing consumer-facing businesses, most recently as President & COO of buybuy BABY, and concurrently as Chief Customer Experience Officer and Head of Business Development for Bed Bath & Beyond. Meka now serves as an operating advisor and board member to a variety of small to mid-sized companies to help them refine their business models, forge strategic partnerships, build deeper customer relationships, and create an aligned organization that can deliver superior operational results.