Q4 2025

Organizations are navigating a maelstrom of rapid technological shifts, evolving work models, and environmental sustainability commitments. Our latest Economic and Business Outlook Survey, developed with Eden McCallum, captures how over 379 global business leaders are responding to this moment of transformation. Their insights reveal a mix of experimentation and optimism: generative AI moving from hype to practice, hybrid work remaining the new normal, and sustainability aspirations colliding with operational realities. Their responses reveal organizations at different stages across these areas, and yet leaders are generally united in their optimism that meaningful progress lies ahead.

Generative AI: We’re still in experimentation mode

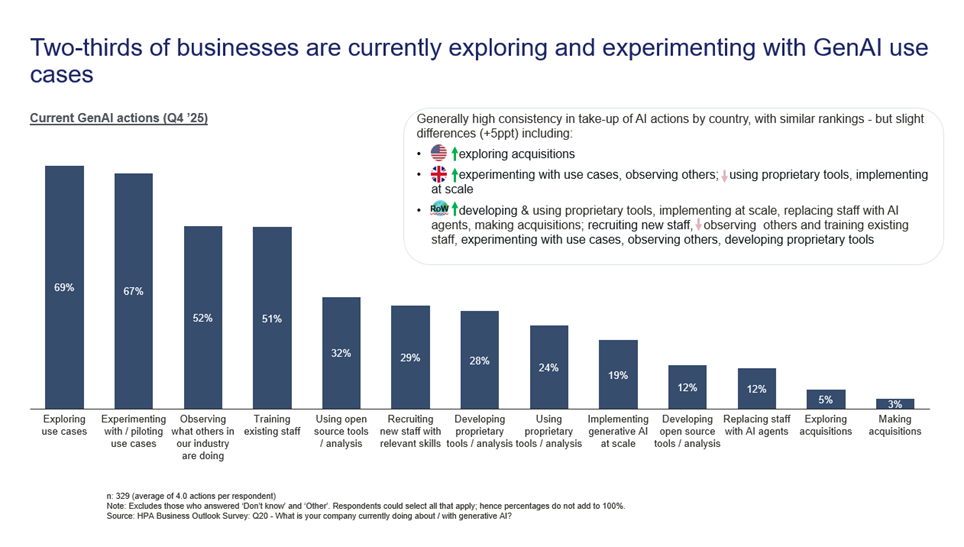

Most companies are still in the early phase of GenAI adoption. Roughly two-thirds are either exploring or experimenting/piloting use cases. Only one-third of businesses are developing or using proprietary tools, and fewer (20%) are implementing GenAI at scale. Approximately half are training current staff, and one-third are hiring new staff with GenAI skills. 12% of organizations have actually replaced staff with AI agents, giving some credence to employee fears around job loss.

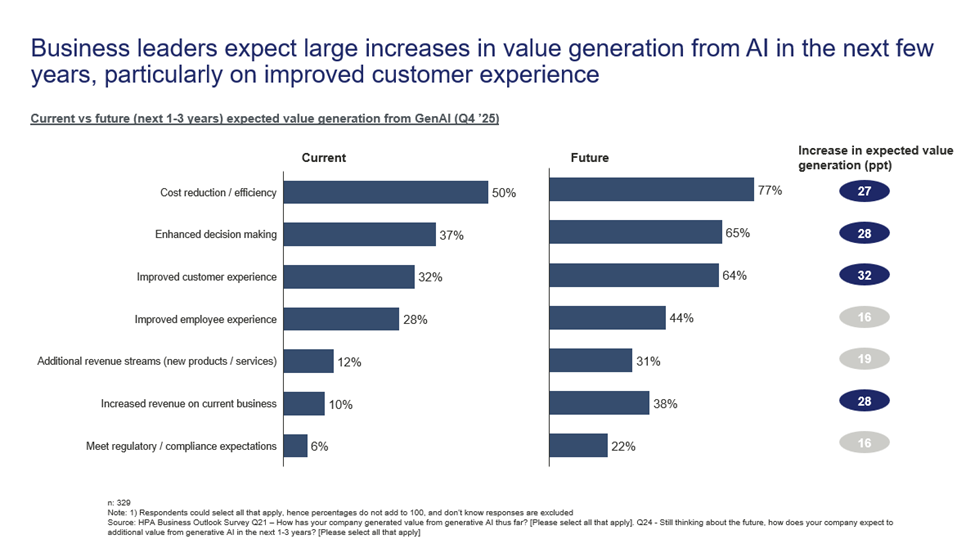

When it comes to ROI, only 10-12% of survey participants indicate direct impact on revenue. But on the flip side, nearly one-third of leaders say GenAI is already making a big impact on their business in some capacity, with over 70% citing the impact as positive. Cost reduction and efficiency improvement (50%) are key benefits of GenAI adoption, followed by enhanced decision-making (37%) and improved customer experience (32%).

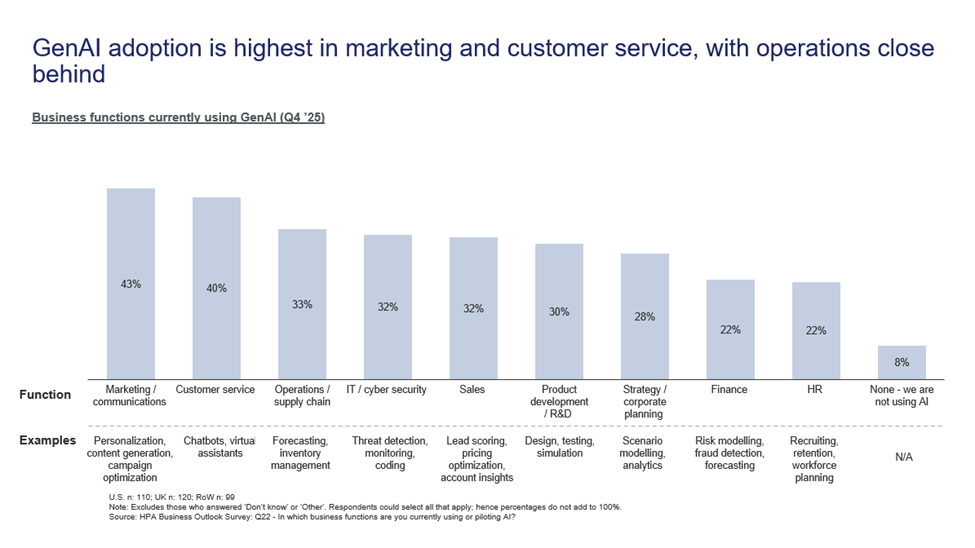

Functionally speaking, the early adopters are marketing and communications (43%), which are using GenAI for content generation, personalization, campaign optimization, and customer service (40%), where chatbots/virtual assistants are the main use case.

Here’s an especially interesting finding: While larger organizations are more active across all GenAI initiatives (exploring more use cases, training more staff, implementing at scale), small companies have reported more positive sentiment about GenAI’s current impact (65% positive vs. 48% for large firms). Given the complexity around implementing GenAI at scale within large organizations, it may be less surprising that when smaller organizations commit to AI, they tend to see a bigger payoff. As one executive noted: “This is the biggest disruption since the beginning of the internet. It allows small players such as ourselves to be as performant as the bigger players.”

In the next 1-3 years, 80% of leaders expect GenAI to have a ‘significant’ or ‘very significant’ impact on their businesses. This is quite an increase from today’s 33%. In the near-term leaders anticipate increased value generation, especially regarding improved customer experience, as well as cost reduction/efficiency gains, increased revenue, and enhanced decision making.

Ways of working: Hybrid is here to stay, but more time in office is expected

Hybrid work continues to dominate ways of working, with nearly 7 in 10 organizations adopting this approach globally. Approximately 10% are still fully office-based and just under 10% fully remote, with the remainder varying their approach “by team”. The U.S. stands out at both extremes, with more fully office-based and fully remote organizations compared to global peers.

Nearly 40% of U.S. office workers have an in-office policy of 4-5 days per week,

compared to 20-30% in the UK and the rest of the world.

Satisfaction with current workplace arrangements is relatively high among leaders, with over two-thirds reporting they are satisfied, citing flexibility, work-life balance, and access to wider talent pools as key benefits of hybrid. As one leader said: “In-office time facilitates collaboration, learning and a way to embed new cultural norms, while the flexibility to work remotely enables us to recruit from a wider talent pool.” Those that are unsatisfied conversely believe that more time in office is needed ‘for skill-sharing, development, and idea generation’ or that full-time in office creates ‘limited flexibility for normal happenings in life’.

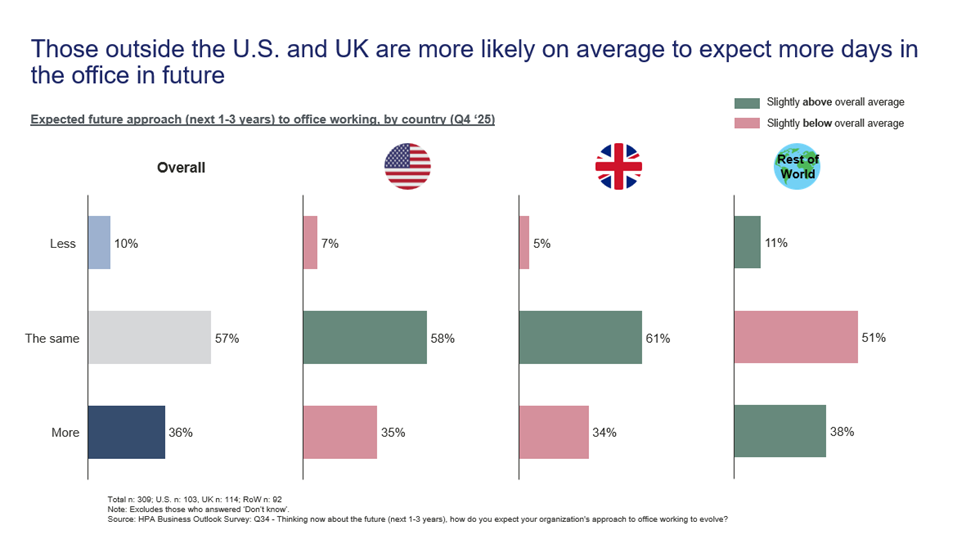

Looking ahead, most organizations (roughly 57%) expect their approach to remain stable over the next 1-3 years, though more than a third (36%) anticipate more time in office will be required (i.e., shifting from 3 days a week in the office to 4 days).

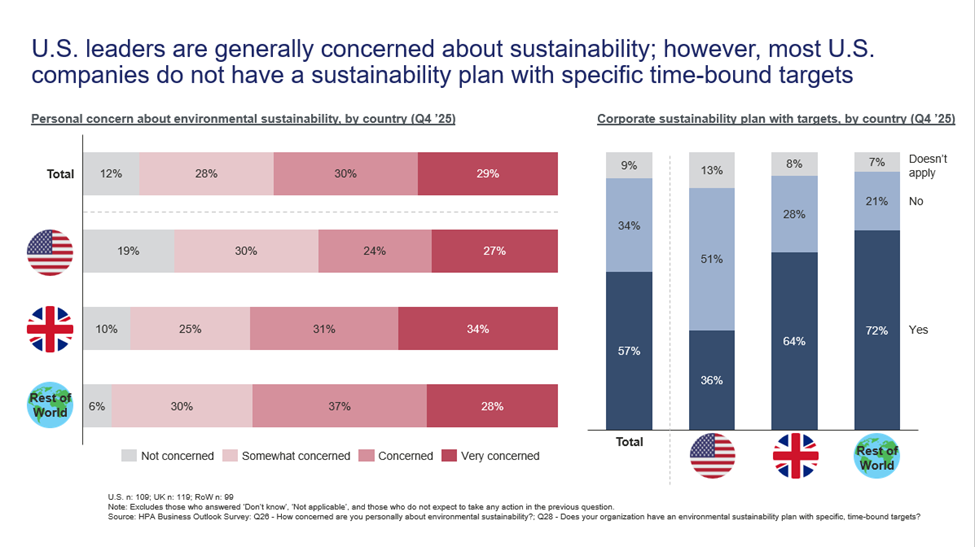

The sustainability paradox: A disconnect between personal concern and corporate targeting

A considerable gap exists between what leaders believe about environmental sustainability personally and what their organizations are doing about it. Globally, 88% of business leaders express personal concern about sustainability, with 29% reporting they are “very concerned.” In the U.S., concern is also high, albeit slightly lower (81%) than the global average.

Despite sustainability being personally important, only 57% of organizations worldwide have a corporate sustainability strategy that includes specific time-bound targets. In the U.S., the figure drops to just 36%. This may come as little surprise, but publicly traded companies and larger organizations (5,000+ employees) are far more likely to have formal sustainability strategies than their private or smaller counterparts.

There’s also notable distance between national pessimism and business optimism, similar to the contrast between leaders’ views on their country’s economic situation (pessimistic) vs. their organization’s (optimistic). Three-quarters of leaders believe their countries achieving net-zero emissions by 2050 is unlikely, with a mere 7% of U.S. leaders feeling optimistic about meeting the target, and 56% feeling very pessimistic. And yet, nearly 70% of leaders globally are optimistic about achieving their organization’s sustainability targets.

Business leaders are juggling a lot right now, from rapid technological transformation to sustainability commitments and evolving workplace expectations. Add global tariffs and general economic uncertainty into the mix, and you would expect widespread pessimism. Instead, what we found was cautious optimism, rooted in leaders’ confidence that their own organizations have a proven ability to adapt. Across regions and sectors, one theme stands out: business leaders may not have all the answers, but they’re betting confidently on their capacity to adapt.

View the survey results below:

hpa-economic-and-business-outlook-survey-q4-2025-2nd-halfThe above is a companion piece to previously published Q4 survey results on leaders’ views of macroeconomics, domestic outlook, and business performance. If you missed it, you can read it here.