Extension mergers, often referred to as roll-ups, have historically been one of the most successful business growth models. Whether pursued to extend geography, markets, products, or some combination of these, such mergers focus primarily on revenue synergies. They have fueled impressive growth for companies like Cisco and IBM, who have used their extensive sales and distribution networks to, in turn, drive sales of products from hundreds of small acquisitions. In addition to their effectiveness in the tech sector, extension mergers have a strong track record of success in the banking, telecommunications, and cable industries through the roll-up of regional players into national entities.

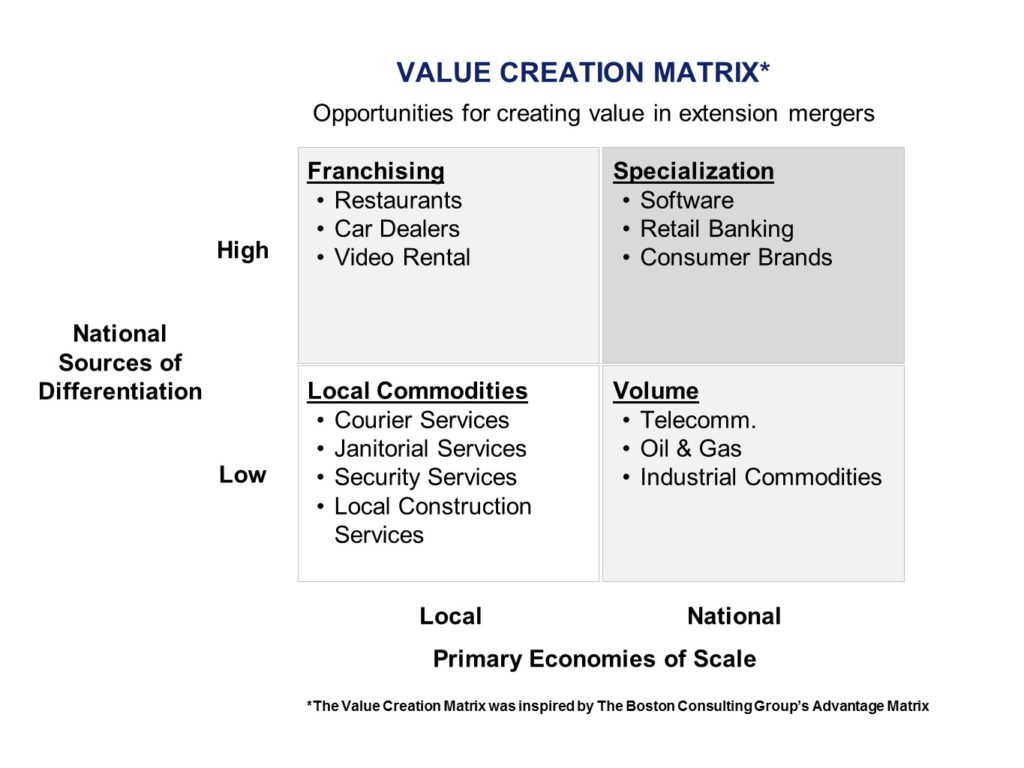

While these mergers have combined non-overlapping products and geographies to generate revenue growth, they have also taken place in industries with high economies of scale at the national level, such as those on the right side of the Value Creation Matrix (below). As a result, they have delivered significant cost synergies from increases in volume on scale-sensitive parts of the cost structure.

We have also seen the formation of national companies–including fast food, video rental stores, and auto dealers (see the upper left-hand corner of Value Creation Matrix)–through franchising. National franchises carve up the cost structure into national and local components. The national franchise consolidates the national scale-sensitive portions of the cost structure and relies on local franchise owners to provide the hustle and hands-on management that local operations require.

Over the past couple of decades, we have seen a noticeable increase in extension merger activity of local commodity businesses, such as couriers, janitorial services, and security services (reference lower left-hand side of Value Creation Matrix). These local commodity sectors have few sources of scale-sensitive costs at the national level and have traditionally been dominated by local players who can outhustle their competition.

Extension mergers that roll up local operating companies.

Roll-ups have a pattern. In the beginning, they create value by increasing liquidity. Small companies have limited access to capital and the company’s stock is usually very difficult to buy or sell, making it illiquid. This depresses the earnings multiple that the company can expect to receive from investors. When a few small companies are rolled up into a bigger company, the bigger company’s stock becomes attractive to more investors. This expands the company’s access to capital and its liquidity. Increased liquidity translates into a higher earnings multiple and greater valuation.

The net net? The bigger company can create financial value by consolidating small companies with low earnings multiples into the larger company that has a higher earnings multiple.

Other roll-ups follow suit and it becomes a race for size. As companies consolidate, this liquidity arbitrage loses its power and the acquirer must find new sources of value to make the consolidation work.

In the early days of this kind of roll-up, investors can make large financial returns. However, the long-term financial results are mixed, with some doing well and others experiencing some type of financial failure or blow-up that destroys shareholder value.

A couple of case studies to illustrate:

Velocity Express, a roll-up of local courier businesses, grew to over 200 locations in the United States before it collapsed from poor financial performance due to failed integration.

Service Corporation International, a funeral home roll-up, matched the S&P performance for its first twelve years, then suffered a stock collapse when its efforts to expand the roll-up internationally failed. The scaled-back company still lags far behind the S&P for total returns.

But it’s not all bleak.

On the positive side, Quest Diagnostics, a roll-up of diagnostic laboratories, has had a much better track record. Since its spin-off from Corning in 1997, Quest has grown from $1.5 billion in revenue to $7.5 billion today. Quest’s stock has also done well, rising by over 2,200% compared to the S&P’s gain of 290%. While Quest likely has more opportunities for regional economies of scale than many local commodity roll-ups, there is something to be learned from Quest’s approach to managing its portfolio of roll-ups for value.

Various companies are now pursuing extension-based roll-ups in other highly fragmented and labor-intensive sectors: Brookdale (assisted living), Kellermeyer Bergensons Services (janitorial services), and Securitas (security services) are a few examples of firms working to crack the code on the lower-left side of the Value Creation Matrix.

There may be rough waters ahead for these companies and others like them, as many of them are singularly focused on getting big fast through aggregation. Questions around how to create operating value, drive profitability, standardize processes, and achieve competitive advantage have likely been deferred. The problem is that these are the questions whose answers determine the long-term viability of the post-roll-up company.

And the overarching question—the billion-dollar question, in fact—is how to transform a group of aggregated local companies into one national or regional enterprise with competitive differentiation and advantage.

Each local entity will likely have its own primary operating constraint that limits performance, and though the constraint may not be unique, it will be different from many other local entities. The company that aggregates, say, 100 local businesses may end up with a portfolio of 20 or 30 operating constraints, each applying to a percentage of the total and each differing by factors like historical practices, location (e.g., different state/local regulatory environments), and market.

There will be winners and losers in every one of these sectors. The winners will be those that get big and create competitive advantage from their growing portfolio of operations. Those who cannot shift from a growth-only focus and find a solution to the disparate constraints of the units that make up the whole will very likely not last.

More on Mergers:

Stay tuned for Part 2 of this article, Extension Mergers: Secrets to Success in Industry Roll-ups. In it, Alex will discuss solutions for creating advantage and driving value. You can also read more about successful mergers in Alex’s white paper, Why Do Intentions Matter in Making Mergers Work?

Alex Nesbitt is a Senior Advisor at HighPoint Associates, a strategy consulting firm headquartered in El Segundo, CA. Alex has 30+ years of management consulting experience and a strong track record of partnering with CEOs to tackle issues related to strategy, organization, senior team management, operational effectiveness, and performance improvement.